- MENU

- HOME

- SEARCH

- WORLD

- MAIN

- AFRICA

- ASIA

- BALKANS

- EUROPE

- LATIN AMERICA

- MIDDLE EAST

- United Kingdom

- United States

- Argentina

- Australia

- Austria

- Benelux

- Brazil

- Canada

- China

- France

- Germany

- Greece

- Hungary

- India

- Indonesia

- Ireland

- Israel

- Italy

- Japan

- Korea

- Mexico

- New Zealand

- Pakistan

- Philippines

- Poland

- Russia

- South Africa

- Spain

- Taiwan

- Turkey

- USA

- BUSINESS

- WEALTH

- STOCKS

- TECH

- HEALTH

- LIFESTYLE

- ENTERTAINMENT

- SPORTS

- RSS

- iHaveNet.com: Investing

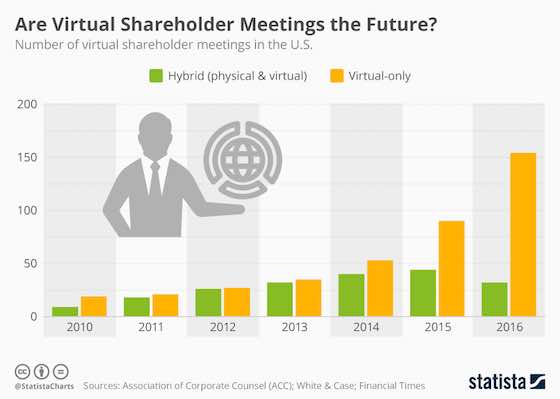

Are Virtual Shareholder Meetings the Future?

by James Saft (Reuters)

The growth in the number of virtual annual shareholder meetings in the United States

U.S. company stock buybacks are down 21 percent in the first seven months of 2016 compared to the same period a year earlier, according to TrimTabs Investment Research, a fall driven in part by five consecutive quarters of year-over-year earnings declines among S&P 500 stocks.

Buybacks, which cancel shares and thus increase per-share earnings, have played a crucial role in supporting the stock market since the financial crisis, flattering earnings even for companies with static or falling revenues.

They, along with dividends, return cash to shareholders, a process often facilitated by borrowed money.

"My biggest concern, which I voiced at the start of the year and continue to worry about, is the sustainability of cash flows. Put bluntly, U.S. companies cannot keep returning cash at the rate at which they are today," Aswath Damodaran, a professor of finance at New York University, writes in his blog.

Over the first six months of the year S&P 500 companies paid out 112 percent of their earnings in the form of either dividends or share buybacks. That, Damodaran argues, is the kind of figure you might expect to see when a recession had suddenly crimped company cashflows, not during a very long-running, if tepid, expansion.

The last time companies were paying out this much more than they are taking in was in 2008, when the financial crisis hammered revenues faster than companies could cut buybacks and dividends.

"Unless earnings show a dramatic growth (and there is no reason to believe that they will), companies will start revving down (or be forced to) their buyback engines and that will put the market under pressure," according to Damodaran.

Facing difficulty in growing top-line revenues, companies have been able to fund outsized cash distributions and buybacks by selling bonds to a market hungry for an alternative to Treasury bonds and their extremely low yields. That same hunger, which has as its underlying cause extraordinary monetary policy, has also driven appetite for equities, as investors felt forced to take on more risk to gain even a modicum of reward.

Rising Debt But Falling Enthusiasm

Companies have issued debt in such size that net debt compared to a standard measure of earnings is now at an all-time high for non-financial companies in the S&P 500, according to data from FactSet, having almost doubled in about five years.

Yet investors seem less enthusiastic about company buyback plans.

A Goldman Sachs basket of companies with the highest share repurchases has underperformed the broader market this year.

Certainly the very idea of buybacks has come under increasing scrutiny. While a share buyback improves per share earnings performance, it is a piece of financial engineering which increases leverage but does nothing to improve a company's product offerings or market position, much less its long-term prospects. Indeed, the vogue for buybacks has happened at the same time as an otherwise puzzling lack of corporate investment, especially given that corporate profit margins are still high by historic standards.

For the buyback boom to truly end, one of two things must happen: companies must think better of it as a strategy, or funds must run short or become difficult to obtain. Even more likely, if money becomes more difficult to come by, the strategy rethink will become more urgent.

Corporate profits are still pretty high as a percentage of gross domestic product, but the trend, at least among the largest companies, is downward. If that carries on, and it clearly can even without the impetus of a recession, payouts must be cut or even more debt will be required.

As of yet, demand for corporate bonds remains strong. Yields on investment-grade U.S. corporate bonds are not far off all-time lows, driven by falling government debt interest rates. Volumes of bonds issued have been healthy too, though this year may see less issuance of corporate debt than last.

One potential problem for the corporate debt boom, and the accompanying buyback binge, would be rising interest rates.

While a return to historically normal rates seems far off, markets are now betting that the Fed makes its second interest rate hike in this tightening campaign in December, the anniversary of its first last year. As interest rates for safer instruments like Treasury bonds rise, the relative attractions of corporate debt and corporate leverage will fall.

Stocks won't enjoy this process but long-term investors, who depend on company dynamism and on overall economic growth, should.

More: How Warren Buffett's Wealth Grew From the 1930s to Today

Investing: "Are Virtual Shareholder Meetings the Future?"