- MENU

- HOME

- SEARCH

- WORLD

- MAIN

- AFRICA

- ASIA

- BALKANS

- EUROPE

- LATIN AMERICA

- MIDDLE EAST

- United Kingdom

- United States

- Argentina

- Australia

- Austria

- Benelux

- Brazil

- Canada

- China

- France

- Germany

- Greece

- Hungary

- India

- Indonesia

- Ireland

- Israel

- Italy

- Japan

- Korea

- Mexico

- New Zealand

- Pakistan

- Philippines

- Poland

- Russia

- South Africa

- Spain

- Taiwan

- Turkey

- USA

- BUSINESS

- WEALTH

- STOCKS

- TECH

- HEALTH

- LIFESTYLE

- ENTERTAINMENT

- SPORTS

- RSS

- iHaveNet.com: Politics

by Arianna Huffington

Madoff accused of $50 billion dollar investment fraud

See if this sounds familiar:

An ambitious and risky undertaking carried out with hubris, and featuring the weeding out of anyone who raises alarm bells, little-to-no transparency, an oversight system in which no central authority is accountable, and the deliberate manufacturing of ambiguity and complexity so that if -- when -- it all falls to pieces, the excuse "who could have known?" can be used . . .

Is it Iraq? Fannie Mae? Citigroup? Bernie Madoff?

The correct answer is: all of the above.

When you look at the elements that were crucial to the creation of each of these debacles, it's amazing how much in common they all have.

And not just in how they began but in how they ended: with those responsible being amazed at what happened, because . . . who could have known?

Well, to paraphrase James Inhofe, I'm amazed at the amazement.

In fact, when historians look for a name that sums up the Bush II years, they could do worse than calling them The "Who Could Have Known?" Era.

Each of the disasters listed above was entirely predictable. And, indeed, was predicted. But those who rang the alarm bells were aggressively ignored, which is why it's important that we not let those responsible get away with the "Who Could Have Known?" excuse.

Let's start with Iraq -- specifically the reconstruction of Iraq.

This weekend the New York Times got its hands on the unpublished 513-page federal history of the reconstruction. It's not pretty. As the Times puts it: It was "an effort crippled before the invasion by Pentagon planners who were hostile to the idea of rebuilding a foreign country, and then molded into a $100 billion failure by bureaucratic turf wars, spiraling violence and ignorance of the basic elements of Iraqi society and infrastructure." As a result, almost six years and $117 billion later, many essential services are only now reaching pre-war levels.

The report quotes Colin Powell on how the Pentagon, to cover up its failures, "kept inventing numbers of Iraqi security forces (that had reached readiness) -- the number would jump 20,000 a week! 'We now have 80,000, we now have 100,000, we now have 120,000.'"

Hmm, making up numbers to realize a short-term gain, but which end up making the inevitable long-term reckoning much worse?

Sounds a lot like what was happening at Citigroup at around the same time.

In late 2002, Charles Prince was put in charge of the Citigroup's corporate and investment bank. The banking giant was already knee deep in toxic paper and aggressively looking the other way.

He was so successful at averting his eyes that when, five years later, as Wall Street began to feel the initial shocks of the mortgage meltdown, he was told that the bank owned $43 billion in mortgage-related assets -- it was the first he'd heard of it. Isn't that something he should have known? Or did he prefer not knowing?

Prince had plenty of help ignoring the obvious, particularly from Robert Rubin.

According to a former Citigroup executive quoted in the long New York Times analysis of Citi's downfall, despite ascending to the top of the Citi food chain, Prince "didn't know a C.D.O. from a grocery list, so he looked for someone for advice and support. That person was Rubin."

When it all came tumbling down, both Rubin and Prince portrayed themselves as helpless victims of circumstance, because . . . Who Could Have Known?

"I've thought a lot about that," Rubin said when asked if he made mistakes at Citigroup. "I honestly don't know. In hindsight, there are a lot of things we'd do differently. But in the context of the facts as I knew them and my role, I'm inclined to think probably not."

What he means, of course, is the facts as he chose to know them.

Prince's head is even higher in the clouds: "Anything," he said, "based on human endeavor and certainly any business that involves risk-taking, you're going to have problems from time to time."

Sounds like he's reading from the same damage control playbook as former Fannie Mae CEO Franklin Raines.

According to Raines, he can't be blamed for what happened at Fannie Mae because mortgage stuff is so, well, complicated. In fact, he can't even understand his own mortgage: "I know I can't and I've tried," Raines told a House committee last week. "To this day, I don't know what it said. . . . It's impossible for the average person to understand" mortgage terms such as negative amortization.

In other words, Who Could Have Known?

Committee chair Henry Waxman wasn't buying it: "These documents make clear that Fannie Mae and Freddie Mac knew what they were doing. Their own risk managers raised warning after warning about the dangers of investing heavily in the subprime and alternative mortgage markets."

Ignoring warning after warning is an essential element of the "Who Could Have Known?" excuse, as are rewriting history and shamelessly disregarding the foresight shown by those who sounded the alarm bells.

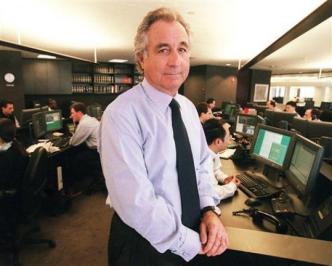

We're seeing the same ingredients in the Bernard Madoff affair.

"We have worked with Madoff for nearly 20 years," said Jeffrey Tucker, a former federal regulator and the head of an investment firm facing losses of $7.5 billion. "We had no indication that we . . . were the victims of such a highly sophisticated, massive fraudulent scheme."

It's a sentiment echoed by Arthur Levitt, the former chairman of the Securities and Exchange Commission: "I've known (Bernie Madoff) for nearly 35 years, and I'm absolutely astonished."

Who Could Have Known?

Well, Harry Markopoulos, for one.

In 1999, after researching Bernie Madoff's methods, Markopolos wrote a letter to the SEC saying, "Madoff Securities is the world's largest Ponzi Scheme." He pursued his claims with the feds for the next nine years, with little result.

Jim Vos, another investment adviser who had examined Bernard Madoff's firm, says: "There's no smoking gun, but if you added it all up you wonder why people either did not get it or chose to ignore the red flags."

The answer comes from Vos's cohort, Jake Walthour Jr., who told HuffPost blogger Vicky Ward: "In a bull market no one bothers to ask how the returns are met, they just like the returns."

Hasn't the "Who Could Have Known?" excuse been exposed as a sham enough times to render it obsolete?

Apparently not. Here come the Bush Legacy Project's revisionists expecting us to believe that everyone thought Saddam had WMD -- even though many were on record saying he didn't.

In the wake of 9/11, Condi Rice assured us nobody "could have predicted" that someone "would try to use an airplane as a missile." Except, of course, the government report that in 1999 said, "Suicide bomber(s) belonging to al Qaeda's Martyrdom Battalion could crash-land an aircraft packed with high explosives (C-4 and semtex) into the Pentagon, the headquarters of the Central Intelligence Agency (CIA), or the White House."

After Katrina, the White House read from the "Who Could Have Known?" hymnal: No one could have predicted that the storm would be a Category 5, and that this could result in the levees being breached. We now know, of course, that plenty of people knew that the levees could be breached and said so before the storm hit.

Then there is Alan Greenspan, who, looking back in October of this year on the makings of the financial crisis he helped create (I mean, that just happened to come out of nowhere), delivered this "Who Could Have Known?" classic: "If all those extraordinarily capable people were unable to foresee the development of this critical problem . . . we have to ask ourselves: Why is that? And the answer is that we're not smart enough as people. We just cannot see events that far in advance."

The only problem is, many people did see events that far in advance.

Unlike Greenspan, I don't believe the problem is that we are "not smart enough as people." As we've seen time after time, smart enough people are all too willing to ignore facts they don't like. Or even worse, they construct oversight systems designed to be ineffective -- and unable to provide to those in power information they don't really want to know.

Much has been made of the smartness of Obama's new team. But I'm hoping that their defining characteristic won't be their IQs but their willingness to confront reality and take responsibility for their decisions.

It's time to say goodbye to the "Who Could Have Known?" era. It's time to know things again. And to know that you know them.

AMERICAN POLITICS

WORLD | AFRICA | ASIA | EUROPE | LATIN AMERICA | MIDDLE EAST | UNITED STATES | ECONOMICS | EDUCATION | ENVIRONMENT | FOREIGN POLICY | POLITICS

Receive our political analysis by email by subscribing here

Tea Party Budget Cuts $9 Trillion | Politics

© Tribune Media Services